Introducing OmniFire - Property-Level Wildfire Risk API for P&C Underwriters and Risk Providers

Why we spent a year talking to fire scientists, modelers, and underwriters before building OmniFire, our property-level wildfire risk API.

Welcome to Ground Truth, OmniGeo’s publication on the intersection of geospatial AI and physical risk — for the people building in Earth observation and the underwriters, asset owners, and risk teams who have to trust them.

What a year of listening taught us

In late 2025, Headwaters Economics, the wildfire analytics firm Pyrologix, and the U.S. Fire Administration set out to take stock of how the industry actually models wildfire risk. They started with more than 150 risk models, narrowed the field to the 59 that met their criteria, and then interviewed 30 of the people who do this work for a living: fire physicists, structural engineers, catastrophe modelers, and insurers.

The experts disagreed about almost everything, from whether physics-based or simplified operational models are the future to how close anyone is to modeling the way fire jumps from one structure to the next. On one point, they converged almost unanimously. As one interviewee put it, “models are only as good as the data inputs.” A field full of people who build models for a living, concluded that the single highest-leverage gap in wildfire risk is not another model. It is a scalable, validated measurement of the physical condition of individual buildings and the land immediately around them.

We did not need the report to tell us that, though it was striking to watch a field arrive at the conclusion we had reached the hard way. One of us lost a home in the Marshall Fire, the suburban firestorm outside Boulder that destroyed more than a thousand structures in an afternoon. Over the past year, we have sat across the table from carriers, MGAs, reinsurance brokers, and catastrophe modelers, and a few themes surfaced in nearly every conversation. Together, they became the brief for the product we are launching today.

The first is that hazard is not the same as vulnerability. The industry has spent two decades getting very good at modeling fuel loads, wind fields, drought, and fire spread, none of which explains why one house on a street burns to the foundation while the one next door is untouched. That difference is vulnerability, and it lives at the parcel level: the roof material, the vegetation within five feet of the wall, the canopy over the eaves, and whether the homeowner actually cleared what they were told to clear. These are measurement questions, not modeling questions, and they have historically been expensive, manual, and nearly impossible to keep up to date.

The second theme was sharper, and it came up most forcefully from the people closest to the underwriting desk. The capability nobody can buy today is dynamic, near-real-time fuel and vegetation moisture, paired with the ability to verify mitigation after the fact. A carrier tells a homeowner to clear the vegetation in Zone 0, the five feet closest to the structure. The homeowner does the work. And then nothing happens, because there is no way to confirm it until the next aerial flyover, perhaps a year away. In a market increasingly required to give credit for mitigation, that blind spot is expensive.

The third theme was about delivery. Almost no one wanted another black-box score. The largest carriers want raw, explainable features for their own pricing models, smaller carriers want a simple number they can act on, and the data providers in between want differentiated inputs to upgrade what they already sell. The lesson was to serve as the measurement layer that feeds everyone else’s models, rather than as another score. And that, every serious buyer agreed, is proven in only one way: correlation with claims, validated against post-fire damage records, such as California’s DINS database, that show which homes actually burned and which survived.

Underneath all of it, regulation is forcing the issue faster than the data can keep up. California’s defensible-space rules under AB-3074 and Colorado’s HB25-182 increasingly require insurers to evaluate the vegetation immediately around a structure, even as regulators warn that carriers cannot act on or non-renew based on an image showing nothing more than cosmetic wear. The market is now legally obligated to understand parcel-level conditions and mitigation, using data that largely does not yet exist at scale.

That gap is the reason we built OmniGeo. And it is the reason we are launching our first product today.

Introducing OmniFire

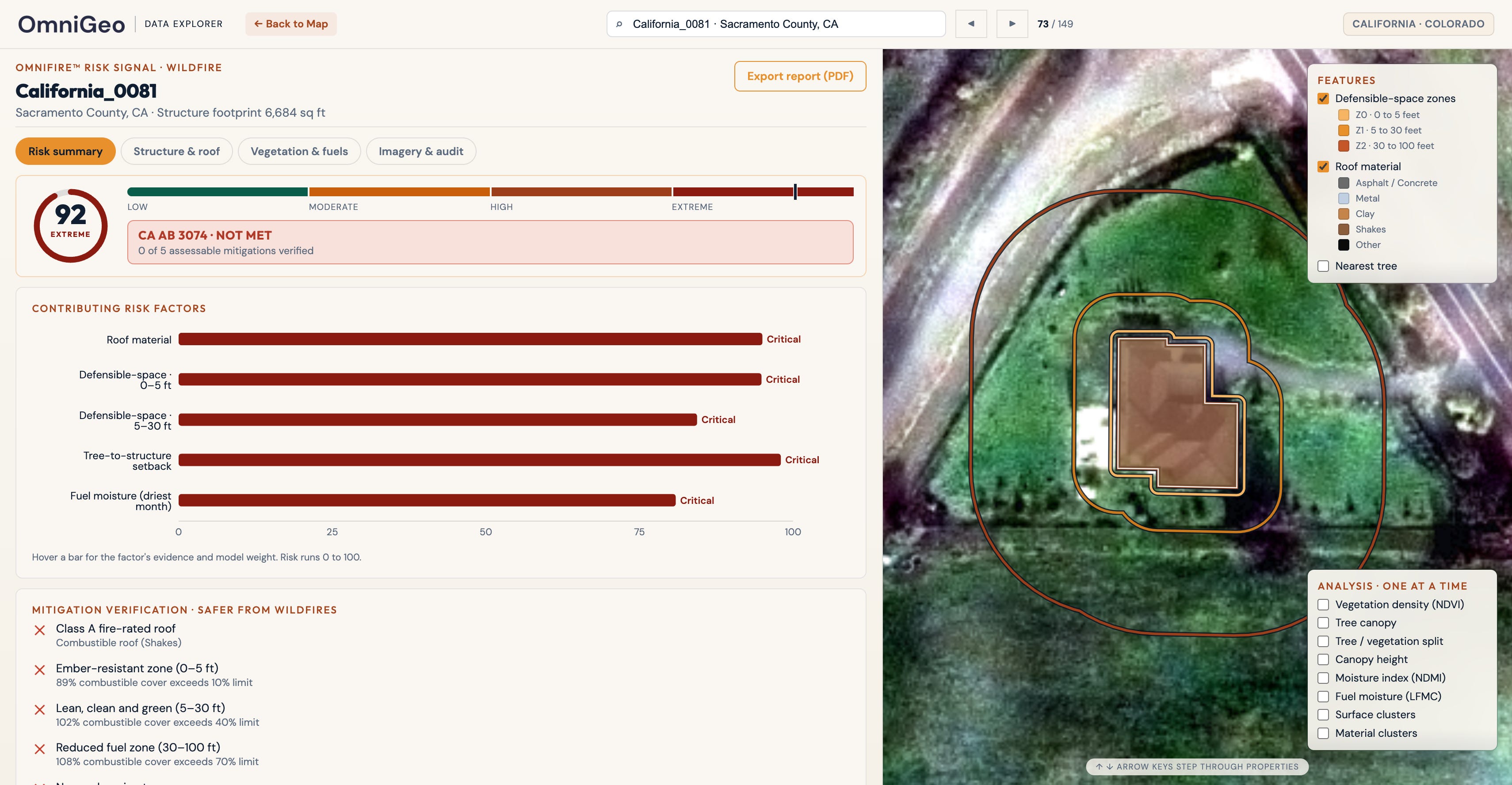

OmniFire is a property-level wildfire risk API for underwriters, MGAs, reinsurers, and the risk platforms that serve them. It is spatial AI for physical risk: it turns frequently refreshed, high-resolution satellite imagery into explainable, parcel-level features that describe how an individual structure is likely to perform when fire arrives. What is the roof made of? How much vegetation surrounds the building? How dry is that vegetation? Is there a canopy hanging over the roof? Does the defensible space around it meet current regulations?

It is built to fill the exact gap the industry described to us. Rather than another regional hazard map, another infrequent aerial flyover, or another costly drone inspection that cannot scale to millions of policies, OmniFire delivers measurements: structured, auditable, and traceable all the way back to the image they came from. Our initial coverage focuses on the California and Colorado counties with the highest wildfire exposure and the densest concentrations of insurable property, with the rest of the western United States to follow.

From Hazard Scores to Material Intelligence

Consider two neighbors. A conventional wildfire hazard map assigns both homes the same regional score because they sit on the same hillside, in the same wind corridor, and are subject to the same drought. But one has a metal roof, a clean perimeter, and well-watered landscaping, while the other has a wood-shake roof, dense brush against the siding, and dry fuel under an overhanging canopy. Their regional hazard is identical. Their vulnerability could not be more different. The hazard map cannot tell them apart, and that distinction, multiplied across a portfolio, is the difference between pricing risk and guessing at it.

OmniFire is built around a single principle that came straight out of those discovery conversations: provide features, not scores. We do not compress a property into one number and ask you to trust it. We deliver the underlying parcel-level observations, roof material, defensible-space vegetation, tree proximity, canopy overhang, vegetation moisture, and more, each one carrying full provenance back to its source image, acquisition date, and processing pipeline. You retain complete control over your underwriting models, pricing, and regulatory filings. We supply the material intelligence that powers them.

What makes that possible is a fundamentally different way of reading imagery. Most computer vision is trained to answer “what is this?” OmniFire is built to answer “what is this made of?”, recovering the physical signal of material, moisture, and condition that ordinary RGB imagery leaves on the table. We will go deep into the science with our co-founder, Dr. Ophir Almog, in a future post. For now, here is what it produces.

What's in the First Release

The first version of OmniFire delivers four core categories of wildfire intelligence, each one a measurement rather than an inference dressed up as a score.

Roof material is one of the strongest single predictors of whether a structure survives a wildfire, and OmniFire classifies the dominant roof material for every building, separating asphalt and concrete, metal, tile, wood, and built-up tar-and-gravel surfaces. This is a signal we validate at roughly 90 percent accuracy against county records, and because it is spectral rather than visual, it correctly identifies two metal roofs of different colors as the same material, whereas an RGB system might call them different.

Defensible-space vegetation answers the question that the new regulations are built around. OmniFire measures vegetation density in the standard defensible-space zones around every structure, reporting separately on Zones 0, 1, and 2, as well as the canopy overhanging the roof. Instead of a subjective field note, an underwriter gets a quantitative, repeatable number for each zone.

Tree density and tree-to-structure distance isolate the fuel that matters most. Trees carry more mass, more canopy, and more ember potential than low vegetation, so OmniFire reports tree canopy coverage by zone, canopy directly over the roof, and the distance from the nearest tree to the building, letting a carrier see not just how much vegetation surrounds a home but how close the dangerous part of it sits.

Vegetation moisture captures flammability over time. OmniFire computes a Normalized Difference Moisture Index from Sentinel-2 imagery to track seasonal water stress and adds a Live Fuel Moisture Content proxy, built from optical, radar, climate, and topographic data, to estimate fuel moisture dynamics throughout the year. Together, they describe ignition conditions, the dynamic layer that the market told us it has been missing.

Every one of these features is delivered with full provenance, traceable to the image, the date, and the pipeline that produced it. And in the validation that this industry trusts most, our signals showed roughly 97 percent agreement with California’s post-fire damage inspection records on which structures survived and which were destroyed, outperforming the standard public datasets.

What's Coming Next

OmniFire is built to expand into a broader spatial AI platform for physical risk, with several capabilities already in development. Near-term additions include tree-specific detection, an expanded roof-material taxonomy, vegetation-change monitoring to verify mitigation over time, roof condition and estimated roof age, deck detection and deck material, ember-resistant hardening features, ladder-fuel identification, and surface-type analysis within the defensible-space zones. Several of these, particularly change monitoring and ladder fuels, came directly out of the discovery conversations, and they point toward the same destination: a continuously updated, parcel-level picture of structural vulnerability and the mitigation that changes it.

Work With Us

If you underwrite or model wildfire risk in California, Colorado, or the broader western United States, we would like to put OmniFire in front of you with a retrospective property test: give us a set of addresses, and we will return parcel-level signals you can compare against what you already know. Let us show you what OmniFire sees at www.omnigeo.ai/omnifire.

The measurement layer behind Ground Truth

OmniGeo’s first product, OmniFire, closes the earth measurement gap for insurers in wildfire-prone areas. OmniFire turns standard imagery into parcel-level measurements of what a property is actually made of, including roof material, defensible space, and fuel moisture. It’s vulnerability measured at scale and it’s live today. If you underwrite, price, or manage wildfire risk, visit www.omnigeo.ai/omnifire to learn more.

|

|